Every morning, roughly 11,200 Americans leave the workforce for good. That figure, repeated daily without pause, adds up to a generational shift in how the country ages out of employment. The data behind it, however, reveals a picture considerably more fractured than the phrase “retirement” tends to suggest.

The most widely cited benchmark puts the average retirement age in the United States at 62 years old. That number comes from a 2024 MassMutual study and has been reinforced by independent surveys across the industry. It represents the actual age at which most workers exit — not the age they planned for, not the age the government targets, and not the age financial advisors recommend. The gap between those figures is where the real story lives.

The distance between wanting to retire and actually being able to

Back in 1991, the average American clocked out for good at 57. The move from 57 to 62 over three decades wasn’t accidental. Policy changes, the slow erosion of defined-benefit pension plans, and the general reality of people needing more money for longer retirements all pushed that number upward. Whether it keeps climbing is an open question, but the short-term data from the Center for Retirement Research at Boston College suggests the trend may be flattening out.

Here’s a number worth sitting with: 59% of Americans surveyed in a 2024 YouGov poll said they want to retire before 65. That’s the preference. What happens in practice runs a few years behind it. For men, the Center for Retirement Research pegged the average actual retirement age at 64.6 in 2024 — three years later than where it stood in 1994, and still short of the 67-year threshold that Social Security defines as full retirement age for anyone born in 1960 or later. Women averaged 62.6 in 2024, a figure that has largely plateaued in recent years.

Receiving SSI or other federal assistance? You could qualify for savings on your phone or internet bill with Lifeline, a federal program supporting eligible households. Learn more: https://t.co/VfqDMkXIPR. pic.twitter.com/1Mya4SWhrv

— Social Security (@SocialSecurity) May 9, 2026

Most Americans retire at 62 — and miss out on $5,108 a month

The Social Security math creates a specific kind of pressure. Claim at 62 and benefits are permanently reduced. Wait until 70 and the monthly check can reach $5,108 — the maximum available in 2025. The average monthly benefit for a retired worker right now sits at $1,981. That gap between $1,981 and $5,108 is entirely a function of when someone files, and most people don’t wait.

Health problems, job loss, caregiving demands — these are the forces that push someone out of the workforce years before they planned, and they show up in the data as a persistent spread between expected retirement age (around 66) and actual retirement age (around 62).

Early retirement, meanwhile, has been going in one direction only. The share of workers leaving between ages 50 and 54 dropped from 9% to 6% over the past two decades. Those exiting at 55 to 59 fell from 19% to 11%. People are staying in longer, partly because they have to, and partly because longer lifespans have changed the math of what a retirement actually costs.

Since 1970, the average retirement period for men has stretched from 12.8 years to 18.6. For women, it’s gone from 16.6 years to 21.3. That’s roughly an extra decade of expenses that the generation retiring today has to fund compared to the one that retired fifty years ago.

What the savings looks like for Americans retiring

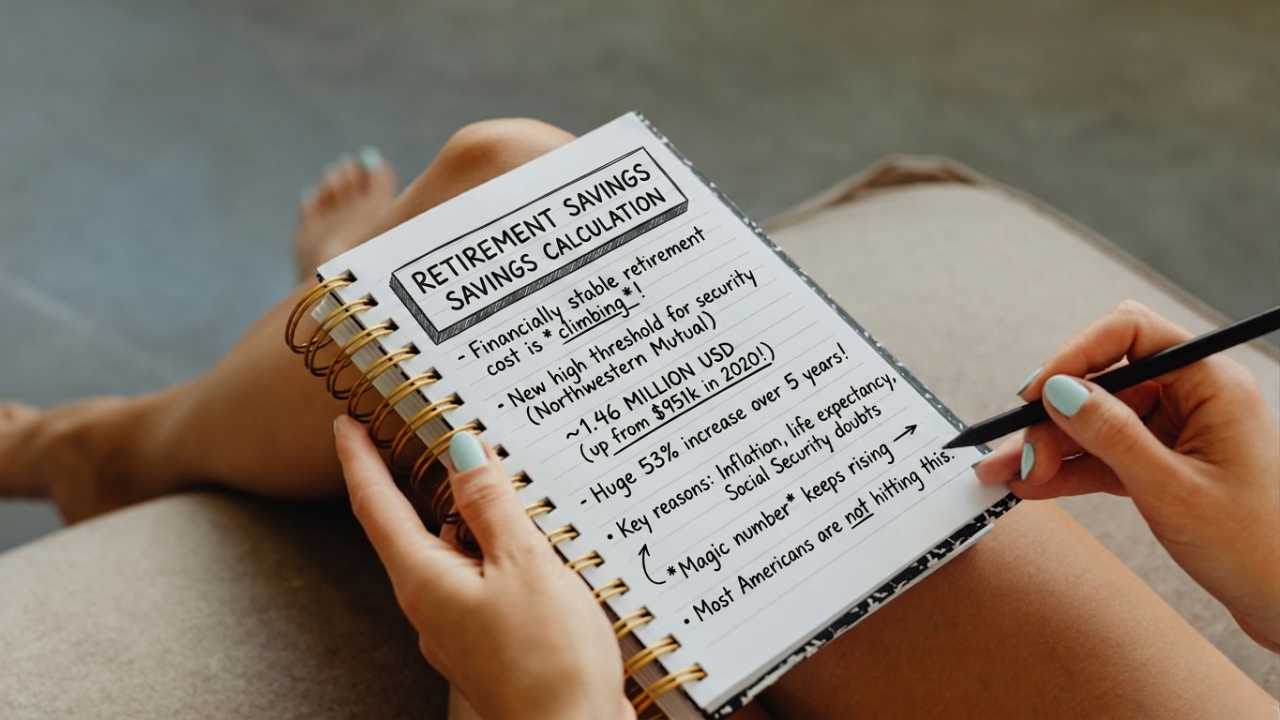

The Federal Reserve’s Survey of Consumer Finances is the most comprehensive source available for retirement savings by age group, and its numbers cut through the noise pretty quickly. For households between 65 and 74 — the core retirement demographic — the average savings figure is $609,230.

The median is $200,000. Those two numbers live in the same dataset and describe the same population, but they diverge so sharply because a relatively small number of very wealthy households pull the average well above where most people actually land.

For the 55-to-64 bracket, the averages and medians follow a similar pattern: $537,560 on average, $185,000 at the median. Fidelity’s Q4 2024 data, pulled from more than 26,700 corporate defined-contribution plans covering 24.5 million participants, showed Baby Boomers carrying average combined balances of $506,302 across 401(k) and IRA accounts.

Vanguard’s 2025 “How America Saves” report — covering nearly 5 million participants in its own recordkeeping system — found a different figure: average account balance of $148,153 at year-end 2024, with participants 65 and older averaging $299,442 and a median of $95,425.

These numbers aren’t contradictory. They’re measuring different things

These numbers aren’t contradictory. They’re measuring different things. The Federal Reserve captures all household retirement assets regardless of where they’re held. Vanguard sees only its own platform participants. Fidelity sees only its own.

The ranges overlap and diverge for structural reasons, but taken together they confirm the same basic pattern: a relatively small share of retirees holds a disproportionate slice of total retirement wealth, and the median figures — the ones that describe where most people actually land — are considerably lower than the averages that tend to appear in headlines.